How Data Creates Massive Leverage in Opaque Marketplaces

The story of Dun & Bradstreet and the insight that led to the birth of one of the oldest data businesses in the US

In August 2025, a private equity firm paid $7.7 billion to take Dun & Bradstreet (D&B) private. It had $2.38 billion in revenue and it has been running continuously for 185 years. Founded in 1841, on the back of a single insight, it is one of the oldest US companies still in existence and arguably the oldest data business.

Before we get to what D&B created, we need to understand the structural tension underlying every opaque market and how that tension gets resolved through data intermediation. We saw the same pattern in the Nielsen Ratings article. And it’s exactly the same one that underlies every major digital marketplace: buyers and sellers who don’t know or trust each other, wanting to transact in mutually beneficial ways.

Let’s dig in.

Timeless problem

Imagine you’re a merchant in New York in 1841. America is expanding westward at a rapid pace. With the opening of the Erie Canal in 1825, a direct water route now connects New York to the Great Lakes and the shipping costs to the Midwest have dropped tenfold.

Traders and storekeepers are pushing into Ohio, Indiana, Missouri. They need trade credit to stock their shelves. And you, a supplier sitting on Hanover Street in Manhattan, need to decide whether to extend it to people you’ve never met.

Side Note: In 1858 the Mercantile Agency (what D&B was first called) found that storekeepers each owed ~$14,500 to wholesalers. Total inter-merchant trade credit in that year was roughly $2.3 billion; nearly half of the entire U.S. GDP in the 1850s.

You now face a huge dilemma. With the expansion comes massive opportunity. If successful, your business will grow and thrive. But at the same time there’s the risk of extending credit to a stranger hundreds of miles away. What if they don’t pay? You lose your shipment, your investment and soon enough your business.

What’s the problem, you say. Just don’t extend credit. Stay local. Well, what if the merchant down the hall is doing it? What if they succeed? You’re playing it safe now but if they get big, they will surely pull more business away from you. You can’t afford to do nothing.

You’re now trapped in a conflict.

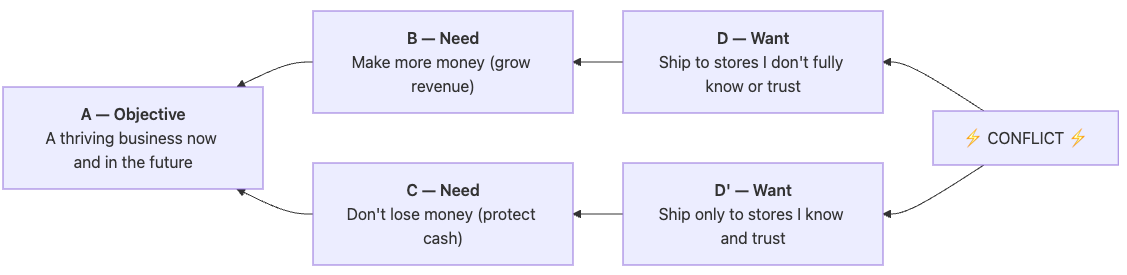

Conflict is at the root cause of every persistent problem so it is in your best interest to learn how to discover it. Let’s verbalize our conflict with the following diagram (called an evaporating cloud diagram):

Core conflict

You read the diagram left to right. The objective is to have a thriving business now and in the future. In order to do that, I need to make more money (grow revenue) and in order to do that, I should ship merchandise to the Midwest to stores and people I don’t fully know or trust.

At the same time, in order to have a thriving business I must make sure I don’t lose money (protect my cash) and to do that I should NOT ship merchandise to stores and people I don’t fully know or trust. This dilemma is specific to the situation merchants faced in the mid-1800s but if we think about it in general terms, it’s a timeless dilemma faced in every marketplace where buyers and sellers transact.

Here’s what it looks like for Nielsen:

Billion dollar insight

According to TOC, conflicts exist because of hidden assumptions that we haven’t checked or verbalized. In this case that assumption is:

Creditworthiness is only knowable through a personal relationship. If you've met the store owner, dealt with him, heard from people who know him, etc you can trust him. If you haven't, you can't.

It is precisely this assumption that Lewis Tappan (D&B’s founder) sought to challenge when he started the Mercantile Agency. His insight was that the information about shop owners the merchants needed didn’t need to come from personal connections. If he could collect it through trusted third parties and transfer that trust to the merchant, it would help everyone involved.

In TOC this is known as an injection.

So he sent out circulars to recruit a network of correspondents (lawyers, bank cashiers, merchants, postmasters, sheriffs, etc). people with community standing, whose word would carry weight, who would report on the creditworthiness of businesses in their region.

And while the information was initially in the form of anecdotes, gossip and hearsay, it served an important purpose. It spoke to the character of the shop owner. The correspondents were asked to report things like: honesty, punctuality, thrift, vices (specifically drinking and gambling), energy, experience, marital status, age, etc.

Fun fact: At one time, Tappan’s correspondents included four future U.S. presidents: Abraham Lincoln, Ulysses S Grant, Grover Cleveland, and William McKinley.

This helped but a second problem popped up. Tappan’s correspondents wrote in prose. Useful, but not easy to compare across businesses. How do you weigh “reliable man, keeps his word” against “drinks some but pays his debts”? You can’t extend credit at scale on narrative alone.

John Bradstreet saw this. In 1851 his competing agency introduced the first standardized creditworthiness score — an alphanumeric rating that reduced every business to the same common language: A letter for financial strength. A number for creditworthiness. Now you can compare two unknown stores in two different states in seconds.

Bradstreet later merged his agency with R.G. Dun & Company to form Dun & Bradstreet after years of intense competition.

Positive feedback loops

How does the creditworthiness score fix the lack of information issue?

One of the first problems any new marketplace company faces (think about AirBnB, Facebook, eBay, etc.) is the so-called “cold start” problem. You have no buyers and no sellers. Assuming you can overcome this, network effects start to slowly compound and the network begins to thrive.

The creditworthiness score is just a proxy for the shop owners’ probability of paying the merchants back. Once they start to make money the growth flywheel starts to spin. They pay merchants back.

More merchants subscribe to D&B and start accepting orders and extending credit to these stores by shipping goods on net-90 terms. More stores, in turn, start making money and paying the merchants back. Meanwhile D&B also grows as it continues to invest in improving the score and expanding their network of correspondents. All parties benefit.

The dilemma Tappan solved applies to every opaque marketplace where buyers and sellers want to transact with scarcr information about each other. Nielsen solved it for advertisers and broadcasters in the 1950s. eBay’s feedback system solved it for online buyers and sellers in the early days of the internet.

Airbnb, Uber, every major digital marketplace today solves it the same way, with data. The question worth asking is what kinds of conflicts exist in your company’s market that data can solve?

That’s it for this issue. if you enjoyed it feel free to like, reply or comment. I read every single one and I love talking to my readers.

Until next time.